Piketty, Saez-Zucman, and the primacy of high progressive taxation

tags: Piketty,Phillip W. Magness,Thomas Piketty,saez,saez-zucman 2014,zucman

Earlier this year I blogged at length about a series of data errors, large and small, in Thomas Piketty’s bestselling book Capital in the 21st Century (a summary of Piketty’s remaining errors may be found here, and an extended discussion of Piketty’s misuse of Soviet Union data assumptions to produce a desired result may be found here).

One of the main issues with Piketty’s data concerned a graph, Figure 10.5, which purported to show a dramatic increase in wealth inequality in the United States over the last 30 years. Scrutiny of this graph by myself and others (see here) called attention to a number of unconventional and suspect data handling decisions as he selectively compiled it from a multitude of sources using widely divergent methodologies. Yet when faced with these criticisms, Piketty opted to sidestep the many problems with his own chart and defer instead to a forthcoming study by his frequent collaborators Gabriel Zucman and Emmanuel Saez that purportedly validated his claimed trend of rapidly expanding wealth inequality. At the time Piketty took cover in its numbers, the public version of the Saez-Zucman “study” existed only in the form of a PowerPoint slideshow, making it inaccessible to further scrutiny. This did not stop a number of prominent economics bloggers including Paul Krugman and Brad DeLong from claiming some amount of vindication in this promised piece of scholarship.

Along with Robert Murphy, I pointed out at the time that the main figure from the Saez-Zucman PowerPoint seemed to suffer from a major data problem: after closely tracking another estimate of U.S. wealth inequality for almost a century (found in a 2004 paper by Saez and Wojciech Kopczuk), their new graph suddenly diverged from a relatively flat trend line sometime around 1984 or 1985, showing that wealth inequality shot dramatically upward thereafter. As the new Saez-Zucman data therefore appeared to be anomalous when considered along side other estimation methods, I accordingly expected that much of the discussion would turn upon the presence of this discrepancy and how they attempt to account for it vis-a-vis previous work.

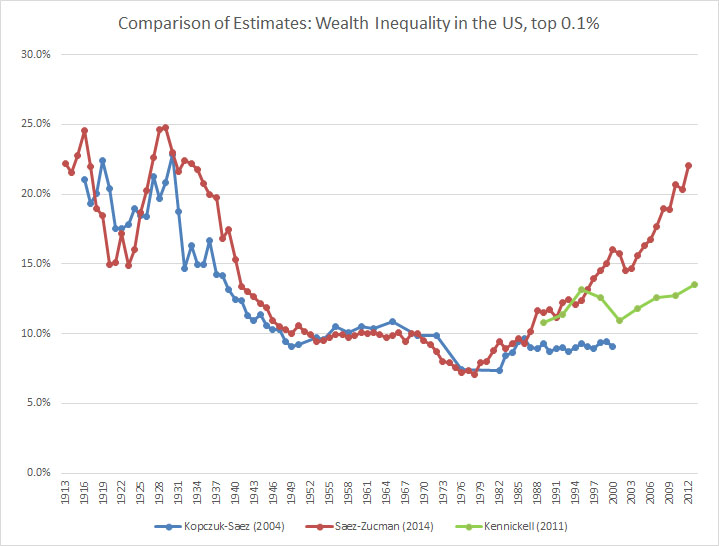

A working draft of the Saez-Zucman paper was released earlier this month and may be accessed here. Needless to say, the anticipated discrepancy is both present and pronounced. I generated the following figure from the data appendix to Saez-Zucman along with two other estimation methods – the estate tax-based data set from Kopczuk-Saez (2004) that runs through the year 2000 and a parallel Survey of Consumer Finances estimate by Kennickell that runs to the present, albeit with less frequency in its data points. As you can see, the first diverges after 1985 and the second after 1994.

The new Saez-Zucman paper attempts to address this discrepancy, albeit briefly, by attributing it almost entirely to a pronounced mortality gradient between the rich and the ultra-rich (stated briefly, they claim the ultra-rich live significantly longer than everyone else, including lesser categories of rich persons). The data set behind this claim is both lightly attested – consisting of a marked trend that is based on mortality statistics across only 6 observation points – and opaquely presented in the paper, being only lightly annotated in its presentation and mostly buried amidst the clutter of their data files. I intend to address it in depth when time permits a closer scrutiny of their spreadsheets, but after an initial read I was left with the impression that they have attempted to tackle a complex subject meriting a thorough examination in its own distinct paper by treating it in the course of a few brief paragraphs, appended somewhat carelessly to the end of their wealth inequality study. I am therefore expecting that a closer examination will reveal that, while probably warranting some consideration, the effect of the claimed mortality gradient for the super-rich on their wealth accumulation vis-a-vis the merely rich has been overstated and oversimplified to fit their new model.

A more pressing matter about this observed divergence in the new Saez-Zucman study warrants immediate attention though, as they have used their new data trend to issue a policy prescription for radically increased progressive taxation in the United States. As stated in an accompanying policy paper issued by Saez and Zucman last week, they liken this trend line to a “return of the roaring twenties”:

“Wealth inequality, it turns out, has followed a spectacular U-shape evolution over the past 100 years. From the Great Depression in the 1930s through the late 1970s there was a substantial democratization of wealth. The trend then inverted, with the share of total household wealth owned by the top 0.1 percent increasing to 22 percent in 2012 from 7 percent in the late 1970s.”

Citing their own results as an imminent and pressing call for corrective action, Saez and Zucman then offer the following policy solutions:

“What should be done to avoid this dystopian future? We need policies that reduce the concentration of wealth, prevent the transformation of self-made wealth into inherited fortunes, and encourage savings among the middle class. First, current preferential tax rates on capital income compared to wage income are hard to defend in light of the rise of wealth inequality and the very high savings rate of the wealthy. Second, estate taxation is the most direct tool to prevent self-made fortunes from becoming inherited wealth—the least justifiable form of inequality in the American meritocratic ideal. Progressive estate and income taxation were the key tools that reduced the concentration of wealth after the Great Depression. The same proven tools are needed again today.” (Saez-Zucman, Washington Center for Equitable Growth, October 20, 2014)

Given the authors’ openly stated affinity for Piketty’s similar conclusions, their proposal for a higher and radically more progressive tax structure is unsurprising. But is this prescription also a justifiable implication of a scientifically sound and impartial investigation of the data? Or do Saez and Zucman and Piketty simply have an ideological disposition toward implementing a high progressive tax structure, which manifests itself in their scholarship irrespective of the data results they obtain?

I’ll venture a suggestion that the latter may well be at play here, and would call your attention to the aforementioned paper that Saez co-authored with Kopczuk in 2004. Recall that Saez’s 2004 study showed a dramatically different trend line (see the blue line in the chart above) for the distribution of wealth in the United States than the new Saez-Zucman estimate (the red line) from 1985 onward. The estimation technique he used at the time showed an almost completely flat trend, whereas the “new” technique shows a sharp upward spike. So how did Saez account for the results he found back in 2004? He credited the observed flat trend line to the effectiveness of progressive tax policy in reigning in wealth inequality, also citing an earlier paper that he co-wrote with Piketty that – at the time – suggested the same interpretation. The relevant passage from 2004 reads:

“In the early 1980s, top wealth shares have increased, and this increase has also been very concentrated. However, this increase is small relative to the losses from the first part of the twentieth century and the top wealth shares increased only to the levels prevailing prior to the recessions of the 1970s. Furthermore, this increase took place in the early 1980s and top shares were stable during the 1990s. This evidence is consistent with the dramatic decline in top capital incomes documented in Piketty and Saez (2003) using income tax return data. As they do, we tentatively suggest (but do not prove) that steep progressive income and estate taxation, by reducing the rate of wealth accumulation of the rich, may have been the most important factor preventing large fortunes to be reconstituted after the shocks of the 1929–1945 period.” (Kopczuk-Saez 2004, emphasis added)

Saez reiterated this observation at several points in the 2004 paper, describing it as “consistent with findings from the Survey of Consumer Finances (Kennickell, 2003; Scholz, 2003), which also indicate hardly any growth in wealth concentration since 1995.” He also interpreted the flat trend line of the 1990s as evidence of a new type of working rich wealth generated in the wake of the internet boom, as distinct from the class of wealthy capital-owning rentiers at the middle of Piketty’s current theory. And while he seemingly questioned the wisdom of 1980s era tax cuts in the 2004 paper, suggesting a possible resurgence in inequality in distant decades to come, Saez in 2004 was quite clearly ready to claim victory for the 20th century’s progressive taxation experiments. As he noted, the 2004 results were “consistent with the decreased importance of capital incomes at the top of the income distribution documented by Piketty and Saez (2003), and suggest that the rentier class of the early century is not yet reconstituted.”

Given the pronounced trend line divergences between Kopczuk-Saez (2004) and Saez-Zucman (2014), Saez’s turn of interpretations amidst conflicting data results is particularly revealing. In 2004 the flat trend line of his observation was a credited product of almost a century of heavy progressive taxation. In 2014 a dramatically opposite “new” trend line, found using a different estimation technique across the exact same period, is now a demonstration that we need…heavy progressive taxation. Given this one constant between two directly opposite results obtained by different attempts to measure the same thing, it seems difficult to avoid the conclusion that the tax hike cart is pulling the data horse around in Saez’s latest inquiry into U.S. wealth inequality.