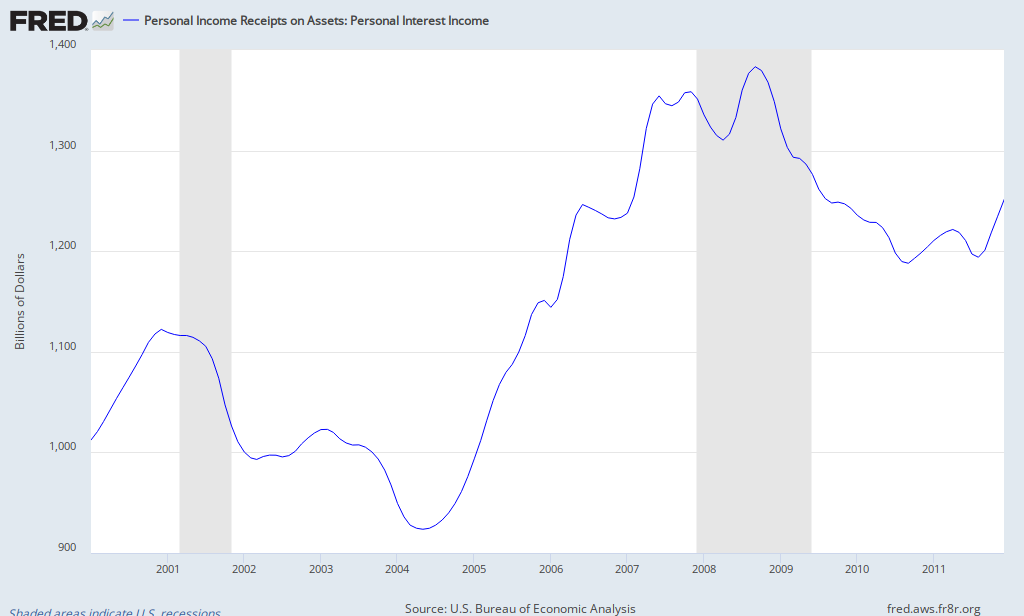

As the graph above shows, personal interest earnings rose substantially from 2004 to 2008, then dropped precipitously when the Fed’s new policies took effect in the last quarter of 2008. During the past year, such earnings have more or less stabilized in the neighborhood of $1 trillion. However, the present amount is approximately the same as the amount that was earned in the year 2000—eleven years ago.

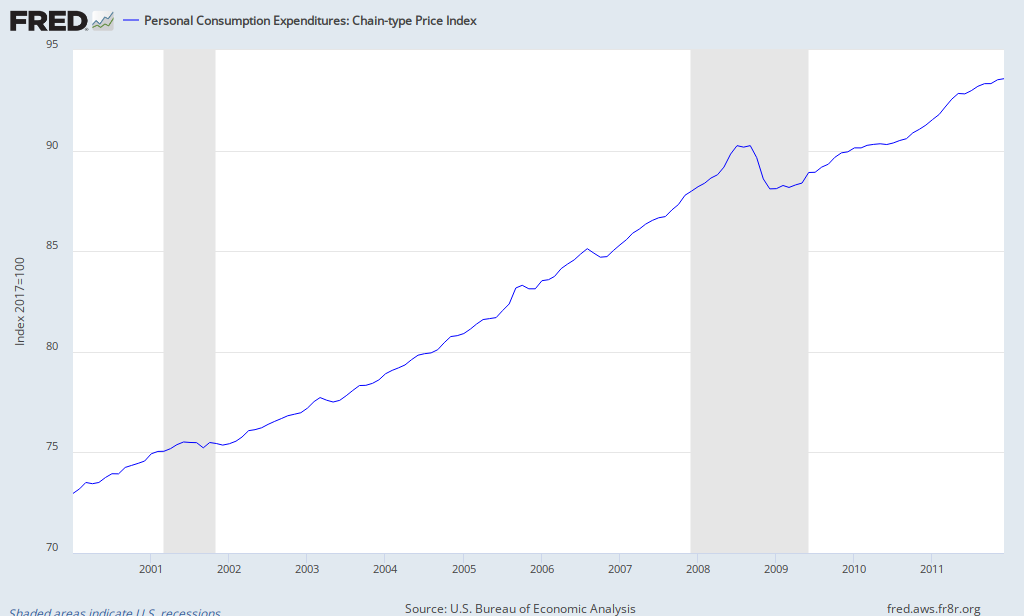

These data, however, are given in nominal dollars, whose purchasing power has declined substantially over the past decade. As the graph below shows, the price index for personal consumption expenditures has risen since 2000 by approximately 28 percent. Therefore, the current flow of personal interest income has purchasing power equal to only about 78 percent of the purchasing power of the personal interest income earned eleven years ago. Of course, the decline since the peak in 2008 has been much greater—in the neighborhood of a one-third drop in real terms.

Defenders of the Fed historically have argued, among other things, that central-bank monetary policies have a sort of neutrality: they affect aggregate demand, the overall price level, and other macroeconomic variables, but they do not attempt to carry out the kind of micromanagement of the economy that Soviet-style central planning attempts. This argument has always been bogus because monetary policy was never—indeed, could not be—neutral. It always had differential effects on different classes of people and different sorts of economic activity, depending in part on who received new infusions of central-bank money first, second, and later in the process and on how these persons’ actions affected ongoing real economic processes. Nonetheless, defenders of the central bank might have argued that at least the Fed did not attempt in any direct way to determine definite changes in the distribution of income, either personal or functional.

Such defenses now ring unmistakably hollow. Even apart from the Fed’s entry into clear credit-allocation activities (e.g., buying mortgage-backed securities rather than Treasury bonds alone), it is plain that the Fed is acting in a way that impoverishes a definite class of persons—those heavily dependent on interest earnings for their income—and, moreover, that a policy of keeping interest rates on low-risk assets near zero must eventually wipe out such persons’ incomes completely. In that event, people who worked and saved over a working lifetime, taking personal responsibility for guaranteeing their self-sufficiency during their elderly, nonworking years, will be able to survive only at the mercy of the providers of private and public charity.

The link between the Fed’s policies and this undeniable effect is too direct and too obvious for anyone, including the Fed’s managers, to overlook or misunderstand. We may only conclude, then, that the Fed’s managers either (1) want to wipe out the retirees and others who rely heavily on interest earnings or (2) consider these people’s immiseration an acceptable price to pay in order to achieve other objectives. Can any decent person approve such policy making?