The Temptation of Bernanke: How Historical Memory Feeds Fed Power

“Tyranny is the exercise of power beyond right.” “Wherever law ends, tyranny begins.”

—John Locke, Second Treatise of Civil Government

“The historian is . . . one step nearer to direct power over public opinion than is the theorist.”

—Friedrich von Hayek

Man of the Year (2009)

Say what you will, but the Fed certainly has chutzpah: driving interest rates to zero, printing money, and now jawboning Congress to write down the principal of the nation’s mortgages (nationalized by force in 2009 and held by the federal government). It’s only money, after all, the property of “nobody” since the government now owns the nation’s housing debt. Bernanke has declared that if Congress does not legislate as he desires, then Bernanke will take law-less action. By Locke’s definition, that is tyranny

Why does the Fed Chairman bother with the facade of lobbying Congress when he assumes unlimited power to himself? Is there any limit to Bernanke’s hubris? Above all, why does he behave this way? A recent Independent Review article splendidly explains the how of Bernanke’s audacious rule but not the why—particularly how he gets away with it.

The answer lies partly in the role historical memory plays in justifying and excusing despotic actions under one man’s rule, particularly during times of crisis. Hayek noted that most policymakers are driven by mental images they got from textbooks, not economic theory. To “sell” a policy or action, the rulers simply resort to historical shorthand passed down from one generation to another, often through government-approved K-12 textbooks and the introductory college text. Don’t kid yourself that they actually teach economics (of any kind) K-16 to the unwashed masses. Instead, it is subsumed—as Hayek knew—via the stories told by historians.

Example: The “script” for the Great Depression goes like this: lack of banking regulation, “unfettered capitalism,” income inequality, and corporate “administered prices” led the nation into a great abyss. FDR came to power, spread the wealth and people felt better. That is still the version in 2011 despite decades of economic literature on the causes of the depression (the role of international gold standard, the Fed’s actions, branch banking bans that weakened the financial system, etc.).

Don’t believe me? Pick up introductory textbooks like Goldfield, et al. The American Journey (2011). The Fed isn’t even mentioned, except as a “Progressive” law that “provided for a flexible national currency and improved access to credit.” “The new system promoted the progressive goals of order and efficiency . . . .” (p. 622). Sure it did.

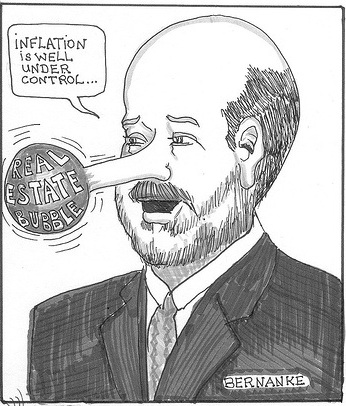

We all know that Ben Bernanke was an economic historian (a line repeated over and over). His knowledge of the depression was more complex than the textbook version (although even he felt compelled to get support by citing the “lessons of history”). Bernanke understood the Fed through Milton Friedman’s eyes and famously promised Friedman that the Fed wouldn’t allow the Great Depression to happen again. Hayek would have faulted Bernanke for reassuring the investing public about the housing bubble. “Nothing to worry about; the fundamentals are strong” was Bernanke’s line. Who remembers that? Here is an apt cartoon from February 2006:

In an illuminating interview (September 17, 2008), Allan Meltzer, the great historian of the Federal Reserve, explained how history—and personal concern for one’s place in it—motivates those in power to arrogate power beyond the letter and spirit of the law.

“I’ve been following these problems for 40 or 50 years. You know, it always comes down at the end to this.

Someone goes to the secretary of the Treasury or, in this case, the chairman of the Fed and says, ‘If we don’t do this, we’re going to have a terrible depression. It’ll be known as the Bernanke depression. And if you don’t act, there’s going to be a disaster.’

Well, that’s not always the case. And these disasters should be headed off early or should be left to the marketplace to settle. They made these mistakes, and they should pay for them.”

A savvy, self-restrained Fed chairman would retort:

“So you say. Tell me, who was chairman of the Federal Reserve between 1929 and 1933?

Answer: Roy A. Young and Eugene Meyer.

Never heard of them? You won’t find them in textbooks or in Hollywood depictions of the depression. In those days, the Federal Reserve “system” was much more fractured and the de facto chair was the head of the New York Fed. Don’t worry, you have never heard of him either: George Harrison (no relation to the Fab Four).

Still, the few people who spend their lives studying the history of money and depressions do remember that the New York Fed had a powerful chairman (Benjamin Strong) but he died and . . . we had a Great Depression because he died. Thus the Great Depression all comes down to the leadership and “expertise” of one man. Or so Bernanke thinks, based on his reading of the Great Depression.

Benjamin Strong’s death “led to decisions, or nondecisions, which might well not have occurred under either better leadership or a more centralized institutional structure.”

“Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.”

Any person who arrogates extreme power to themselves “to do good” ought to be handed a copy of Marcus Aurelius’s Meditations. Aurelius was the Roman emperor-philosophy who reminded his readers that no one remembers the actions of individuals who are constantly in the news of their day. Today, historians pick and choose who will enter the pantheon of “those to be remembered” but they have focused on presidents, leaders of social movements, and little else. You will look in vain for any scapegoating of individual Fed chairman. Instead, the history textbook goes like this: the Progressives came along (circa 1900-1920) and created many agencies to create order and benefit “the People.” They created the Federal Reserve and then . . . the Fed did various (unnamed) things. Now on to the Roaring Twenties and the evils of Wall Street....”

While the mainstream media revels in the presidential horse race, Bernanke is lauded for “doing something” (in general, historians give high marks to those who “do something”—the bigger, the better). And thus Bernanke was Time magazine’s man of the year in 2009 because he “stopped another Great Depression.” This is the left-liberal glow of one-man rule:

“His creative leadership helped ensure that 2009 was a period of weak recovery rather than catastrophic depression, and he still wields unrivaled power over our money, our jobs, our savings and our national future. The decisions he has made, and those he has yet to make, will shape the path of our prosperity, the direction of our politics and our relationship to the world.”

But fear not: historians won’t attribute the cause of this recession to the Fed, Fannie Mae, Freddie Mac or anything but Wall Street and income inequality (remember the “script”). Bernanke was “Man of the Year” in 2009 but in the grand scheme of things he won’t rank so high. The “Man of the Year” two years into the Great Depression was Pierre Laval. Never heard of him? He sold France out to the Nazis, deported Jews to death camps and was executed by firing squad. But that was 15 years after he was named “Man of the Year”!

As for the Fed, it will augment its power and continue to abuse history for its purposes. It is almost inevitable since nearly all Americans have been told the same story of the Great Depression—and future Fed chairmen will take all power to themselves to prevent another one. The press approves but they liked Laval too.

By any other name, one-man rule of a nation is still tyranny. Not that the historians will notice.